DST Plus™ — The Deferred Sales Trust Strategy

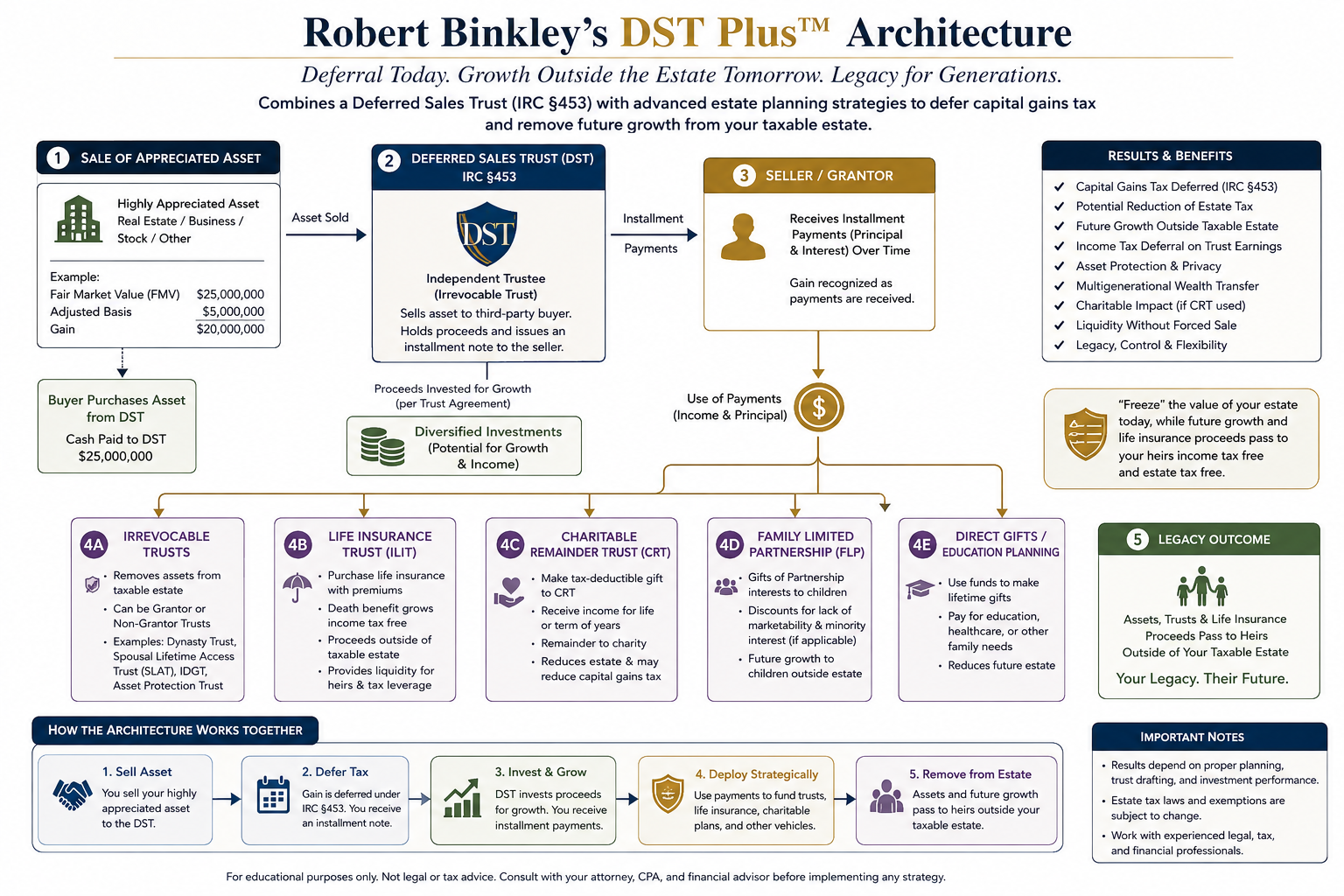

Deferral today. Growth outside the estate tomorrow. Legacy for generations. The DST Plus™ architecture combines a Deferred Sales Trust (under IRC §453) with advanced estate-planning strategies to defer capital gains tax on the sale of a highly appreciated asset and remove future growth from your taxable estate.

Note on terminology. Here “DST” means Deferred Sales

Trust — an installment-sale strategy under IRC §453. That is a different

structure from the Delaware

Statutory Trust (also “DST”) used to hold replacement property in a 1031

exchange, which is covered separately on this site.

How the architecture works together

- Sell the asset. You sell a highly appreciated asset — real estate, a business, stock, or other property — to the Deferred Sales Trust rather than directly to the buyer.

- Defer the tax. An independent trustee (an irrevocable trust) sells the asset to a third-party buyer and issues you an installment note. Under IRC §453, gain is recognized — and tax paid — only as installment payments are received.

- Invest and grow. The trust invests the proceeds for potential growth and income per the trust agreement, and pays you principal and interest over time.

- Deploy strategically. Payments can fund estate-planning vehicles — irrevocable trusts, an Irrevocable Life Insurance Trust (ILIT), a Charitable Remainder Trust (CRT), a Family Limited Partnership (FLP), or direct gifts and education planning.

- Remove from the estate. Assets, trusts, and life-insurance proceeds pass to your heirs outside of your taxable estate — freezing today’s value while future growth accrues to the next generation.

Potential results & benefits

- Capital gains tax deferred (IRC §453)

- Potential reduction of estate tax

- Future growth outside the taxable estate

- Income tax deferral on trust earnings

- Asset protection & privacy

- Multigenerational wealth transfer

- Charitable impact (if a CRT is used)

- Liquidity without a forced sale

- Legacy, control & flexibility

For educational purposes only. This is not legal or tax advice. Results depend on proper planning, trust drafting, and investment performance, and estate-tax laws and exemptions are subject to change. Consult your attorney, CPA, and financial advisor before implementing any strategy.